DEFI FUNDAMENTALS

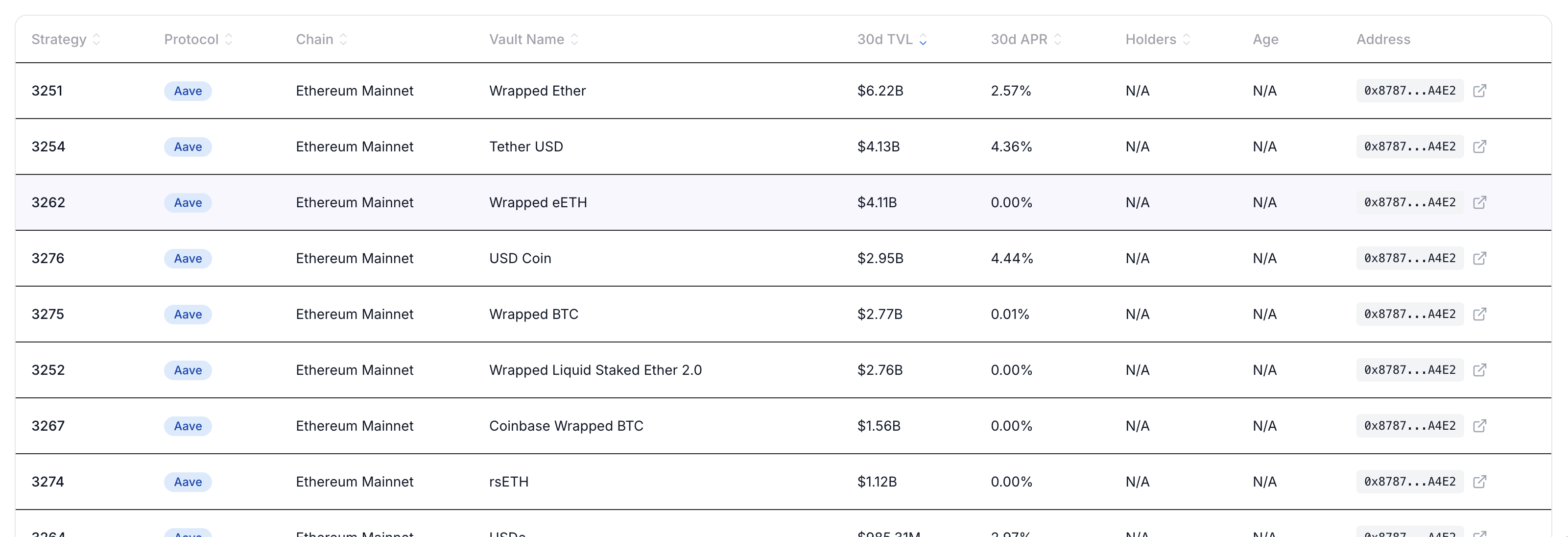

Aave: 0% APR, but $4B in TVL?

An Aave pool with near-zero deposit APR and billions in TVL looks irrational at first glance. It isn't. Most of those depositors are not chasing yield — they are buying borrowing power. Here's how collateral demand decouples APR from TVL on lending markets.

This is a follow-up to Aave TVL: Two Ways to Measure. That article explained why Aave's TVL can be reported two different ways. This one explains a related puzzle: why a pool can show almost 0% APR and still hold billions in deposits.

Data referenced in this article is as of 02.05.26.

The puzzle

At first glance, an Aave pool with almost 0% deposit APR and billions of dollars in TVL looks irrational.

Why would users deposit Wrapped eETH into Aave if the yield is close to zero?

The answer is simple: many users are not depositing Wrapped eETH to earn yield. They are depositing it to use as collateral.

1. Aave is a credit market, not just a yield product

Aave is often viewed as a place to "deposit and earn," but that is only one part of the protocol.

Aave is primarily a lending and borrowing market. Users can:

Supply assets Borrow assets Use supplied assets as collateral Manage leverage or liquidity

So when someone supplies Wrapped eETH, they may not care much about the Wrapped eETH deposit APR.

They may care about what Wrapped eETH allows them to do:

Deposit Wrapped eETH → use it as collateral → borrow USDC or another asset

In this case, Wrapped eETH is not being used as a yield asset. It is being used as borrowing power.

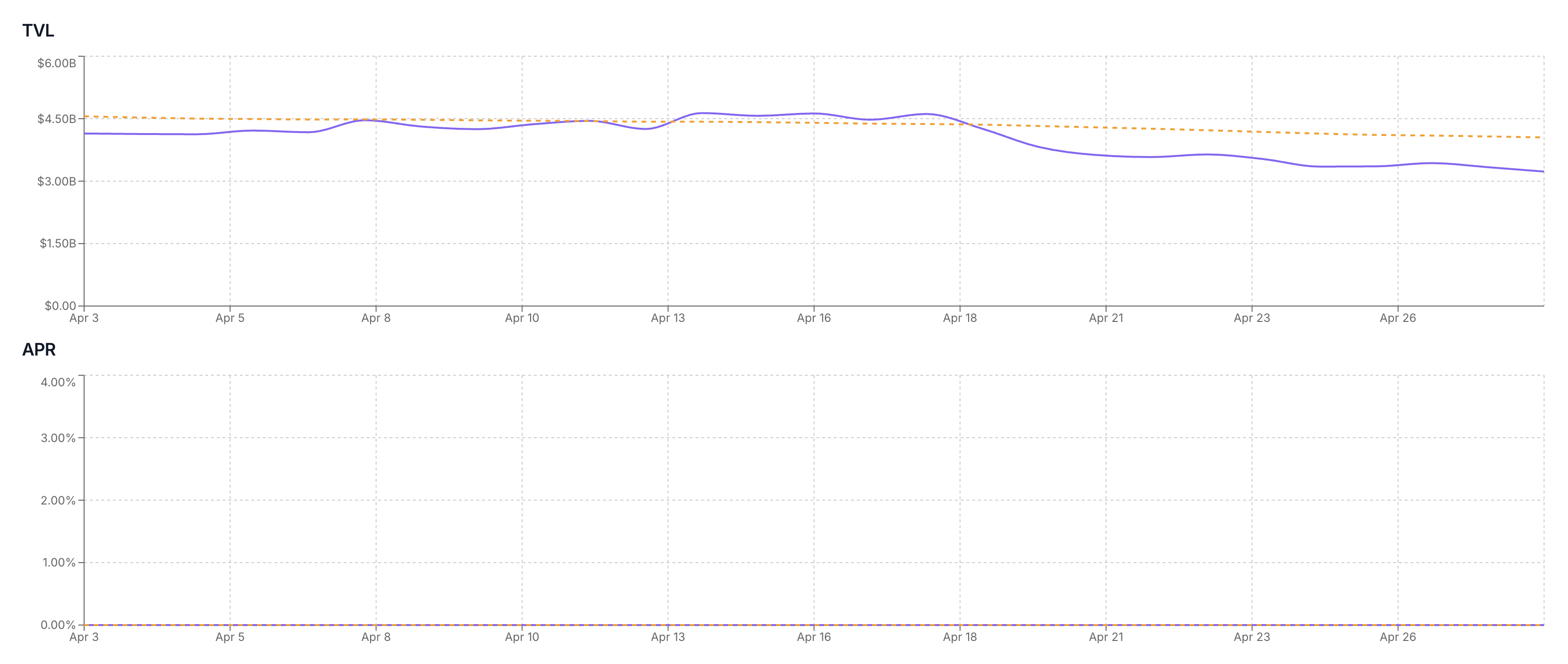

2. Why the Wrapped eETH deposit APR is almost zero

Aave supply APR depends on demand to borrow that same asset.

For Wrapped eETH suppliers to earn meaningful yield, other users need to borrow Wrapped eETH and pay interest on it.

A simplified formula is:

Supply APR ≈ Borrow APR × Utilization × (1 - Reserve Factor)

So if a lot of Wrapped eETH is supplied but only a small amount is borrowed, utilization is low.

Low utilization means low supply APR.

That is why Wrapped eETH can have:

Large deposits Low borrowing demand Low utilization Almost zero deposit APR

This does not mean the pool is unused. It means Wrapped eETH is not heavily borrowed as an asset.

3. The main reason users deposit Wrapped eETH: collateral

The most common reason to supply Wrapped eETH to Aave is to borrow something else.

For example:

User deposits: $1,000,000 of Wrapped eETH User borrows: $400,000 of USDC

The user now has USDC liquidity while still keeping ETH exposure.

This can be useful if the user wants to:

Avoid selling ETH Keep upside exposure Access stablecoin liquidity Use capital elsewhere Create leverage Manage short-term cash needs

The user may earn almost nothing on Wrapped eETH, but that is not the point.

They are effectively paying for a crypto-backed credit line.

4. Why USDC borrow interest does not increase Wrapped eETH APR

This is an important detail.

If a user deposits Wrapped eETH and borrows USDC, the interest they pay is USDC borrow interest.

That interest goes to USDC suppliers, not Wrapped eETH suppliers.

Each Aave asset has its own reserve:

Wrapped eETH reserve → Wrapped eETH supply APR and Wrapped eETH borrow APR USDC reserve → USDC supply APR and USDC borrow APR

So if many users deposit Wrapped eETH and borrow USDC, the result may be:

Wrapped eETH TVL: high Wrapped eETH APR: low USDC borrow demand: high USDC supplier APR: higher

This is why a Wrapped eETH pool can have billions in deposits but almost no deposit yield.

The demand is for Wrapped eETH as collateral, not necessarily for borrowing Wrapped eETH.

5. What the high TVL actually means

A high Wrapped eETH TVL does not mean users are happily chasing 0% yield.

It means many users trust Wrapped eETH as collateral inside Aave.

So the correct interpretation is:

Low Wrapped eETH APR = low demand to borrow Wrapped eETH High Wrapped eETH TVL = high demand to use Wrapped eETH as collateral

This is why APR alone can be misleading.

A pool can have near-zero deposit APR and still be economically important because it provides:

Collateral utility Borrowing power Stablecoin liquidity Portfolio flexibility Leverage infrastructure

The real question is not:

"Why would anyone earn 0%?"

The better question is:

"What can users do with this asset once it is supplied?"

For Wrapped eETH on Aave, the answer is clear:

Users deposit Wrapped eETH because it gives them borrowing power while allowing them to keep ETH exposure.

That is why an Aave pool can show almost 0% APR and still have billions in TVL.

Combined with the methodology question covered in Aave TVL: Two Ways to Measure, this is most of what you need to read an Aave market correctly: TVL is gross deposits, APR reflects borrow demand for that specific asset, and the two numbers do not need to move together.

Related reading

Aave TVL: Two Ways to Measure

Why pigi.finance and DeFiLlama report different Aave TVL numbers — and what each one actually answers.

Understanding DeFi Yield Sources

Lending, liquidity mining, staking, RWAs and more — every category of DeFi yield, explained.

What is a Vault in crypto?

ERC-4626, AMM pools, stability pools — pigi's unified definition of a Vault.