DEFI FUNDAMENTALS

Aave TVL: Two Ways to Measure

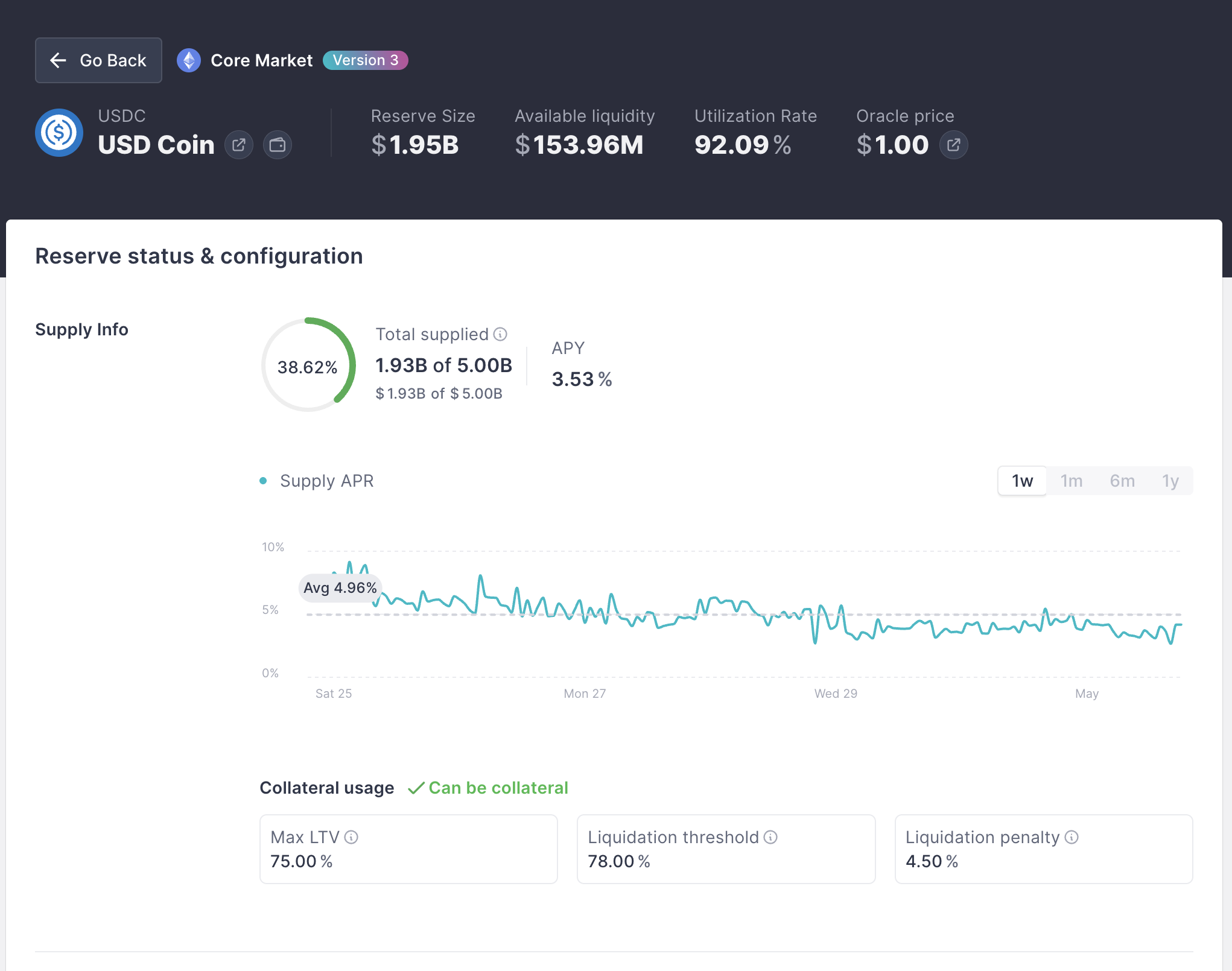

Aave's USDC reserve has $1.93B supplied, $1.78B borrowed, and $153M available (as of 01.04.26). Different dashboards pick different numbers and call them all "TVL". Here's why pigi.finance and DeFiLlama disagree, and what each number actually answers.

Two ways to measure Aave TVL

In DeFi lending markets, the word TVL can mean different things depending on what a dashboard is trying to measure.

This becomes especially visible with Aave. For example, an Aave USDC reserve may have (as of 01.04.26):

Total supplied USDC: $1.93B Total borrowed USDC: $1.78B Available liquidity: $153M

At pigi.finance, we show the TVL of an Aave asset as gross deposits — in this example, about $1.93B.

DeFiLlama's yield pages, however, may show a much smaller number — around $153M — because they are closer to showing available liquidity, calculated roughly as:

Available liquidity = total supplied - total borrowed

Both approaches can be useful. But they answer different questions.

How Aave lending markets work

Aave is built around liquidity pools and individual asset reserves. A reserve is an instance of a token within a liquidity pool, with its own supply data, borrow data, collateral parameters, utilization, and interest rates.

When users supply assets to Aave, those assets can earn interest and can also be used as collateral. Borrowers can then borrow other assets against that collateral, as long as their position remains overcollateralized.

So every lending reserve has three important numbers:

| Metric | Meaning |

|---|---|

| Gross deposits / total supplied | Total amount users have supplied to the reserve |

| Total borrowed / active loans | Amount borrowed from that reserve |

| Available liquidity | Amount still sitting in the reserve and available for new borrows or withdrawals |

Using the USDC example (as of 01.04.26):

Gross deposits: $1.93B Borrowed amount: $1.78B Available liquidity: $153M

All three numbers are true. The difference is what each dashboard chooses to call "TVL."

DeFiLlama's approach: TVL as available or net liquidity

DeFiLlama generally excludes active loans from TVL by default for lending protocols. Their stated reason is to avoid TVL inflation from looping strategies, where the same capital is deposited, borrowed, redeposited, and counted multiple times.

This is a very reasonable concern.

Imagine a user does this:

1. Deposit 100 USDC 2. Borrow 80 USDC 3. Deposit that 80 USDC again 4. Borrow 64 USDC 5. Deposit that 64 USDC again

A gross-deposit view might show:

Total supplied: 244 USDC

But the user originally brought only:

100 USDC of external capital

So from DeFiLlama's perspective, counting all supplied assets as TVL can overstate how much fresh liquidity entered the protocol.

This is why DeFiLlama's lending methodology is conservative. It tries to avoid double-counting borrowed capital as new TVL.

What DeFiLlama's approach is good for

DeFiLlama's method is useful when the question is:

How much liquid capital is still available in the protocol?

or:

How much non-borrowed liquidity remains?

This is especially important for users who care about immediate withdrawal capacity or how much liquidity is still available for new borrowers.

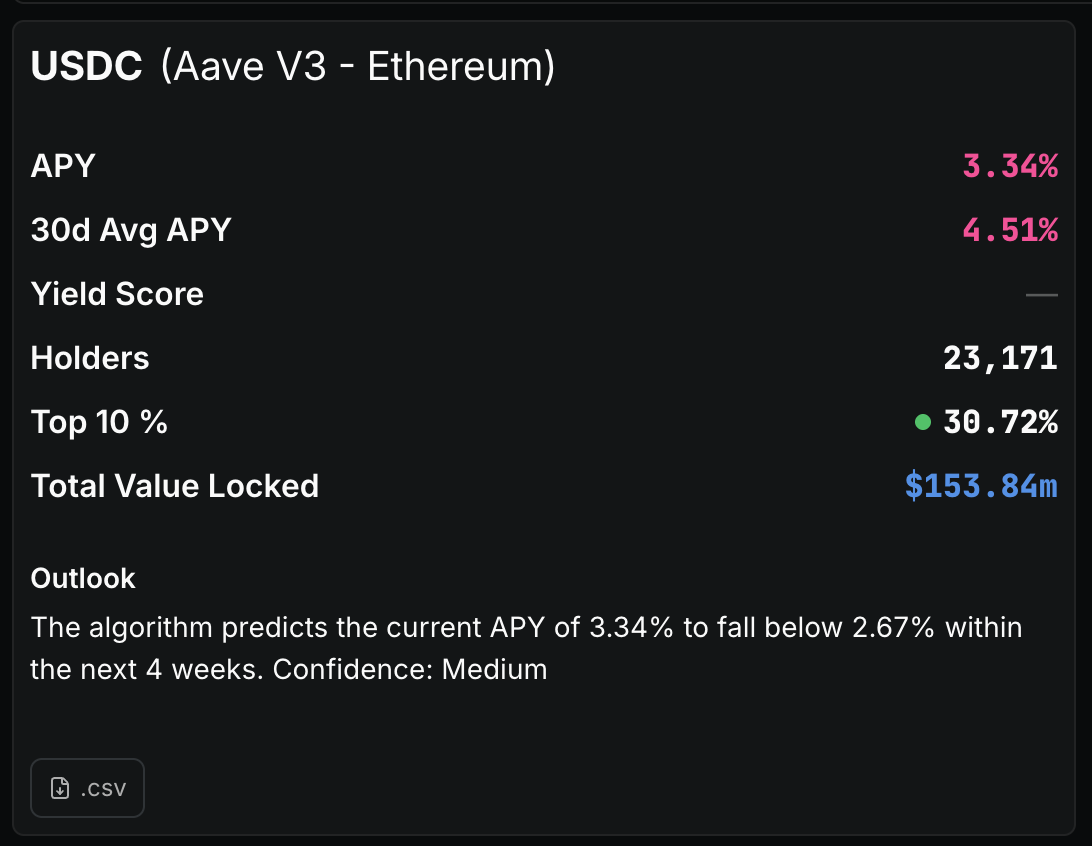

So if a USDC reserve has $1.93B supplied but $1.78B borrowed (as of 01.04.26), then the immediately available USDC is not $1.93B. It is closer to $153M.

That is the strength of DeFiLlama's approach.

pigi.finance's approach: TVL as gross deposits

At pigi.finance, we show Aave asset TVL as gross deposits.

In the same example (as of 01.04.26), we would show:

Aave USDC TVL = $1.93B

not:

Aave USDC TVL = $153M

Why?

Because gross deposits answer a different and very important question:

How much of this asset have users actually supplied to Aave?

For many users, this is the more intuitive meaning of TVL. If users have deposited $1.93B of USDC into an Aave reserve, then the reserve has attracted $1.93B of supplied capital. Even if most of that capital has been borrowed, suppliers still have claims on the pool through their aTokens.

Gross deposits are also important for understanding:

market size supplier exposure collateral base protocol risk user confidence asset-level adoption

If a WBTC reserve has billions in supplied WBTC but almost no available liquidity, the low available liquidity tells one story. But the gross supplied amount tells another: many users trust Aave enough to use WBTC there as collateral.

The key difference

The disagreement is not really about math. It is about interpretation.

DeFiLlama asks:

How much liquidity is still available after loans are removed?

pigi.finance asks:

How much capital have users supplied to this asset reserve?

Both are valid.

But they should not be mixed without explanation.

Related reading

Aave: 0% APR, but $4B in TVL?

How an Aave pool can show near-zero deposit APR with $4B in TVL — when collateral demand decouples APR from deposits.

Understanding DeFi Yield Sources

Lending, liquidity mining, staking, RWAs and more — every category of DeFi yield, explained.

What is a Vault in crypto?

ERC-4626, AMM pools, stability pools — pigi's unified definition of a Vault.